Establishing and adhering to a personal budget is a foundational element of sound financial management. This document outlines a systematic approach to creating a simple yet effective monthly budget, designed for individuals seeking a structured method to track income and expenses. The primary objective is to provide a clear financial roadmap, enabling better decision-making and facilitating the achievement of financial goals.

1. Income Assessment: Quantifying Your Financial Inflow

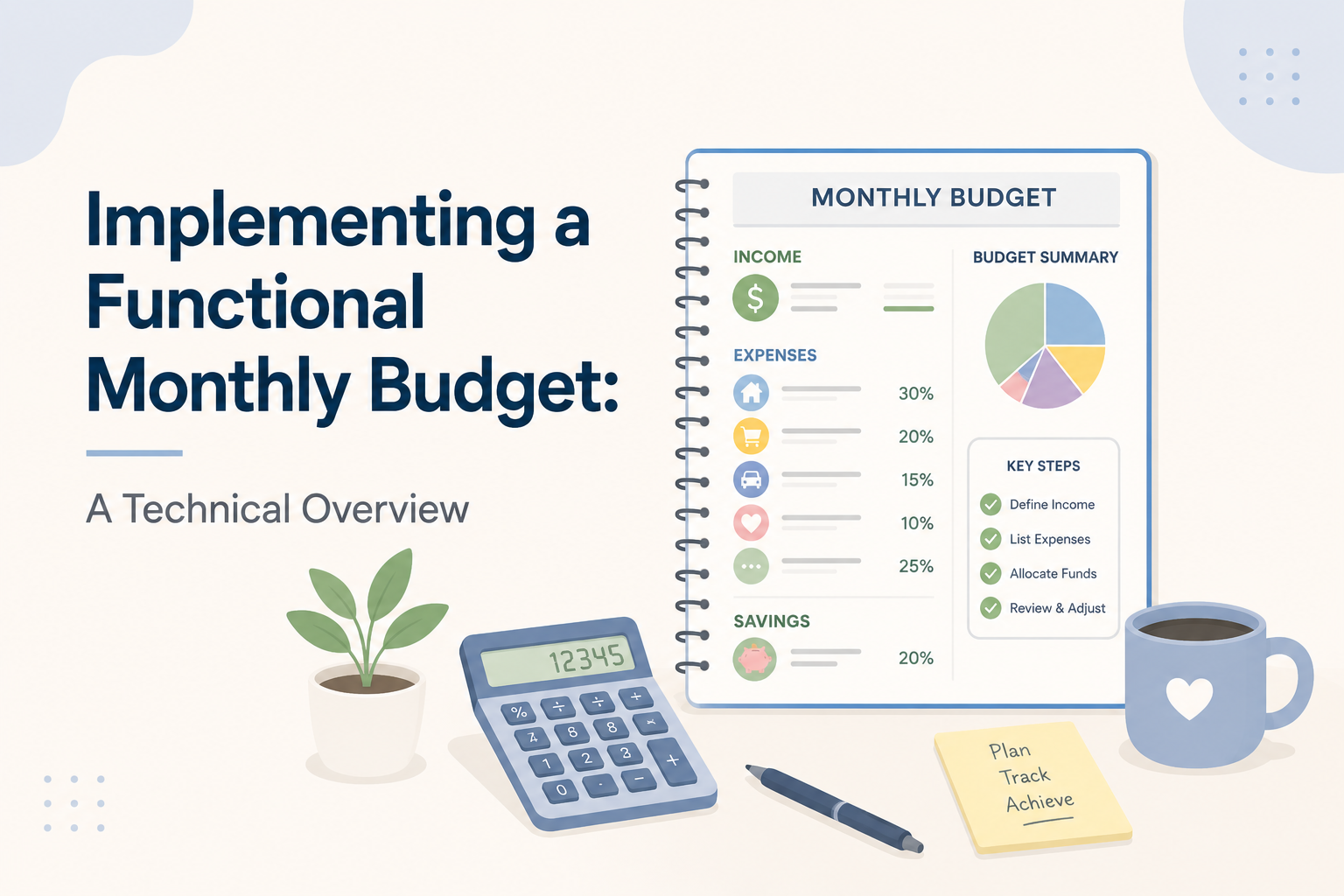

The initial step involves a comprehensive evaluation of all anticipated income streams for the month. This includes regular salary deposits, freelance earnings, rental income, and any other predictable financial inflows. It is crucial to calculate the net income after taxes and deductions, as this represents the actual disposable capital available for allocation. For individuals with variable income, it is advisable to use a conservative average or the lowest anticipated amount to ensure the budget remains realistic and sustainable.

2. Expense Categorization and Tracking: Mapping Your Outgoings

The subsequent phase requires the meticulous identification and categorization of all monthly expenses. These can be broadly classified into two primary groups: fixed expenses and variable expenses.

- Fixed Expenses: These are costs that remain relatively consistent each month and are often non-negotiable. Examples include mortgage or rent payments, loan repayments (car loans, student loans), insurance premiums, and subscription services (e.g., internet, streaming).

- Variable Expenses: These costs fluctuate based on usage and lifestyle choices. Common examples include groceries, utilities (electricity, water, gas – though often somewhat predictable, they can vary seasonally), transportation (fuel, public transport fares), dining out, entertainment, and personal care items.

Utilizing a spreadsheet or a dedicated budgeting application is highly recommended for accurate expense tracking. Recording every transaction, no matter how small, provides invaluable data for analysis and adjustment.

3. Budget Allocation and Reconciliation

Once income and expenses are quantified, the next step is to allocate the net income across the identified expense categories. The principle of “paying yourself first” should be incorporated, prioritizing savings and debt repayment before discretionary spending. A popular budgeting framework recorded and analyzed by experts is the 50/30/20 rule, where 50% of net income is allocated to needs, 30% to wants, and 20% to savings and debt repayment. However, this ratio can be adjusted based on individual financial circumstances and objectives. Regular reconciliation of the budget is paramount. At the end of the month, compare the actual spending in each category against the allocated amounts. This process reveals areas where overspending or underspending occurred, providing critical insights for future budget modifications.

4. Monitoring and Adjustment: The Dynamic Nature of Budgets

A budget is not a static document; it is a living tool that requires ongoing monitoring and periodic adjustments. Throughout the month, diligently track your actual spending against your allocated amounts for each category. Utilize budgeting apps, spreadsheets, or even a simple notebook to record transactions. Regular review (weekly is often recommended) allows you to identify any discrepancies or overspending early on. If you consistently overspend in a particular category, you may need to re-evaluate your allocation or identify strategies to reduce spending in that area. Conversely, if you consistently underspend, you can reallocate those surplus funds towards savings, debt reduction, or other financial goals. This iterative process of monitoring and adjustment is what transforms a simple spending plan into a truly functional financial management system.

5. Goal Integration: Aligning Spending with Aspirations

A truly functional monthly budget is intrinsically linked to your broader financial goals. Whether you are saving for a down payment, planning for retirement, or aiming to eliminate debt, your budget should serve as a mechanism to actively work towards these aspirations. During the allocation phase, ensure that savings and debt repayment are treated as non-negotiable line items, much like fixed expenses. Regularly reviewing your progress towards these goals within the context of your budget reinforces motivation and provides a tangible measure of your financial success.

FAQs

Q1: What is a “functional” monthly budget?

A: A functional monthly budget is one that is practical, actionable, and effectively guides your spending to align with your income and financial goals. It’s not just a list of numbers but a dynamic tool for financial management.

Q2: How do I handle variable income when creating a budget?

A: For variable income, it’s best to be conservative. Use a conservative average of your income over several months or, even better, use the lowest anticipated income amount. This ensures your budget remains realistic and you don’t overcommit based on fluctuating earnings.

Q3: What are the best tools for tracking expenses?

A: Popular tools include budgeting apps (e.g., Mint, YNAB, PocketGuard), spreadsheet software (e.g., Microsoft Excel, Google Sheets), or even a traditional pen and paper notebook. The best tool is the one you will consistently use.

Q4: How often should I review and adjust my budget?

A: It’s recommended to review your budget at least weekly to track spending and identify any immediate issues. A more comprehensive review and adjustment should occur monthly, before the start of the next budgeting period.

Q5: What if I consistently overspend in a category?

A: If you consistently overspend, you have two primary options: either find ways to reduce your spending in that category or reallocate funds from another category that you underspend in. If neither is feasible, you may need to reassess the realism of your initial budget allocations.

References:

“The Total Money Makeover” by Dave Ramsey – A popular guide to personal finance, emphasizing budgeting and debt reduction.

“Your Money or Your Life” by Vicki Robin and Joe Dominguez – Explores the relationship between money and life energy, promoting conscious spending.

Consumer Financial Protection Bureau (CFPB) – Offers resources and tools for budgeting and financial planning. (www.consumerfinance.gov)

You might also like:

Founder and writer of Wex Insights. Joshua Brillante publishes practical, research-based articles on personal finance, productivity, leadership, and personal development. As Wex Insights continues to grow, he also shares travel insights that encourage lifelong learning, better decision-making, and meaningful personal growth. Learn more about the author